Explaining the loan process

A simple guide to the loan application process?

What does the journey look it?

You’re probably wondering how you get from making that initial enquiry with your Zuu Money Finance Specialist to finally settling your new home loan. From the outside it can look like a complicated process, but the good news is, it doesn’t have to be.

Your initial chat with a Zuu Money Finance Specialist is the perfect opportunity for us to get to know you so we can get a good understanding of what you need right now and what your financial goals may be for the future.

For you, it’s a chance to ask all the questions you have about finding and choosing a loan, applying, the approval process, and what happens after that.

Your Zuu Money Finance Specialist is with you every step of the way, giving comprehensive guidance and support to help you achieve your financial goals.

Get started online or contact us for help

How the buying process works

Step 1 - Arrange pre-approval

If you haven’t started your property search, or are still looking, a pre-approved loan can be useful. It gives you a clear picture of what your buying limit is and gives you peace of mind that if you find a property you’re really interested in you can move quickly to make an offer.

Getting pre-approved may also put you in a stronger negotiating position than other potential buyers who don’t have pre-approval. Of course, even with a pre-approval, a "subject to finance clause" is an important protection in any sale contract.

Step 2 - Find your property

Make sure you do plenty of homework when you’re on the hunt for a new property. Research property prices in the area, potential capital growth and existing and planned infrastructure, such as roads, public transport, schools and shops. If you’re unfamiliar with property values in the area, consider a full valuation carried out by a registered valuer before making a final decision.

Step 3 - Make an offer and sign contract

Whether you buy property at auction or make an offer on a listing you’ll be asked to sign a Contract of Sale. This contract will confirm the selling price as well as any terms and conditions. You will need to include appropriate conditions such as subject to finance approval, a building inspection report and a pest inspection.

The period from signing a Contract of Sale to settlement – when the property becomes legally yours – is usually six weeks (shorter in some states, such as Queensland).

Even if you have a pre-approved loan, your lender will still need to complete a valuation of the property you have chosen before issuing full approval and if that valuation is not satisfactory the lender may not give final approval of a loan to purchase that property.

Step 4 - Appoint a conveyancer

You will need a conveyancer or solicitor to act for you to complete the sale. Your conveyancer should also check all rates and taxes have been paid, check land use or building approvals for the property and order any relevant searches.

On settlement day, the conveyancer will check the correct amount of money has been transferred from your lender to the seller and all fees – such as Stamp Duty – are paid, so you can take legal ownership of the property.

Step 5 - Pay your deposit

A deposit is required once a Contract of Sale has been signed by both parties. You won’t yet have access to your home loan, so your deposit will need to come from savings or elsewhere. You may also be able to arrange a deposit bond until settlement.

Step 6 - Cooling off period

If you didn’t buy your property at auction, you may have a cooling off period when you can cancel the contract, although there may be a small penalty. Cooling off periods don’t necessarily apply in every state so check with your conveyancer to find out what your rights may be.

Step 7 - Unconditional Approval

Subject to valuation and any outstanding credit conditions the lender will provide unconditional finance approval for the purchase. It's at this time, subject to satisfying any finance clause within your contract of sale, that your contract will progress too unconditional. It's always recommended that you seek guidance from your conveyancer when dealing with matters involving your contract.

Step 8 - Pre-settlement preparation

It's during this time that you prepare yourself for the settlement. This involves signing your mortgage documents and other required forms, obtaining the correct insurance, and preparing your deposit which is often transferred to your conveyancer's trust account. Being well prepared ahead of settlement will save a lot of tears, trust me.

Step 9 - Settlement day

On settlement day your conveyancer will coordinate the transaction and ensure all parties in the transaction are correctly paid. Settlements often occur in the afternoon. You will be notified by your conveyancer once settlement has been affected, then you are the proud owner of the new home.

Remember that settlement is not guaranteed. There are a host of issues that can occur on the day which can delay settlement. It's important to have a contingency plan in place if you are planning to move into the property on the day of settlement.

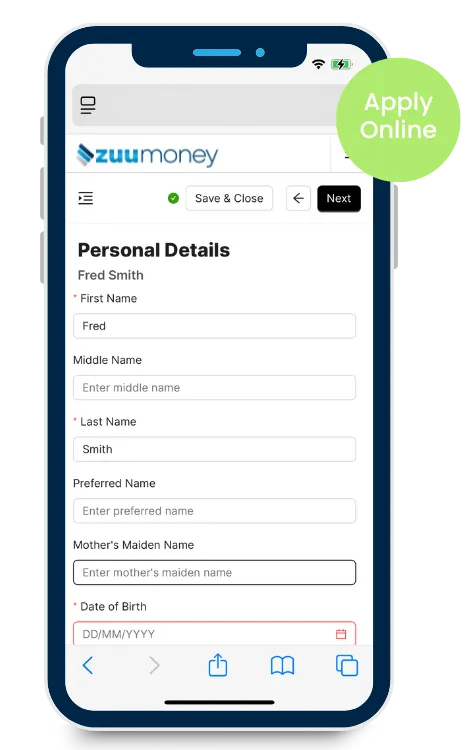

Our smart technology makes applying easy

Applying for you next home loan has never been easier. The Zuu Money online application system allows you to enter your details from any device and upload your documents with ease.

Say goodbye to handwritten application forms and endless emails, all your information is collected in our simple, easy to use platform that saves you time and frustration.

You can get started online or contact your local Zuu Money Finance Specialist for assistance.

Apply from the comfort of your home

Avoid running from bank-to-bank or inviting strangers into your home. The Zuu Money online application process is a breeze and all from the comfort of your home.

1

Initial Discussion

We'll hold a brief conversation with you over the phone or in person to confirm your lending requirements and set you up in our online application system

2

Apply Online

Applying for a home loan is a breeze. Simply enter your details into our online application system and upload your supporting documents.

3

Choose your loan

We'll prepare a customised loan proposal for you from our wide panel of lenders and contact you to discuss your options and answer any questions you might have.

4

Loan Submission

We'll submit the loan application to the lender of your choice and manage the application right through to settlement, keeping you updated along the way.

Featured Product

6.09%

PER ANNUM

Variable*

6.11%

PER ANNUM

Comparison Rate^

Or up to

$3,000

Cash Back

A fully flexible, fee free home loan!

Variable rates offer great flexibility with unlimited extra repayments and free online redraw. Contact Zuu Money today to see if a variable rate home loan is right for you.

Hundreds of loans from Australia's top lenders

You don't need to run from bank-to-bank to find the best deal. Our team of mortgage specialist will compare hundreds of loans from Australia's top lenders and present you with a range of options that suit your lending needs.

A service worthy of 5 stars

* Discounted rate available for owner occupied on Principal and Interest repayments with minimum loan size >$150,000 with borrowings <70%LVR. Rate subject to change without notice. Lender credit criteria, fees and charges apply. Zuu Money Pty Ltd does not endorse any particular lender. A product will be recommended based on your personal financial situation.

^ Comparison rate is calculated on a loan amount of $150,000 for a term of 25 years based on monthly repayments. Different amounts and terms will result in different comparison rates. Costs such as redraw fees or cost savings such as fee waivers, are not included in the comparison rate but may influence the cost of the loan.

Become a Broker

Zuu Money Pty Ltd ABN 66 670 119 105, Australian Credit Licence Number 567690.

Lender credit criteria, fees and charges apply.

The Zuu Money logo is a registered trademark of Zuu Money Pty Ltd. All rights reserved 2026.

| Terms and Conditions | Privacy Policy | Complaints