Bad credit home loans

You're more than a score

Home loan solutions for individuals with adverse credit

What is bad credit and how to understand it

If you have ever failed to make payments on your bills, credit card, mortgage, or any other type of debt in the past, you may have experienced what is known as bad credit. This term refers to a history of difficulties in meeting your financial commitments. This could involve a recurring pattern of late payments as well as more serious occurrences such as defaults or bankruptcy. These events can have a negative impact on a person’s credit report, which lenders consider when evaluating loan applications.

The following are some factors that lenders take into account as indicators of bad credit:

Poor credit conduct: Adverse entries on your credit file such as defaults, bankruptcy, court judgements, or excessive credit enquiries can cause concerns, but they do not automatically disqualify you from obtaining a mortgage.

Unpaid taxes: If you have unpaid tax bills, lenders will take these into consideration. Some lenders may allow for unpaid taxes to be consolidated into your home loan.

Payment arrears: Lenders may be cautious if you have a history of payment arrears on your current loan facilities. Payment arrears is often an indication that a person is struggling financial.

Company/Trust debts: If you are a director of a company that is facing financial difficulties, this may raise concerns about your personal financial position.

Excessive debt: Having too many debts or a negative net worth can often lead to financial hardship. Lenders often apply metrics to measure the amount of debt a person has compared to their income level.

Having a poor credit score can make the process of obtaining a home loan more challenging, but it does not necessarily mean it is impossible. In Australia, a credit score that falls below 500 is categorized as poor credit. Different lenders have different risk appetites for applicants with bad credit. By receiving proper guidance and developing a well-planned approach, getting a home loan is still an attainable goal.

Home loan options for adverse credit

Lenders who offer home loan products to people with bad credit are know as “non-conforming lenders”. These lenders will assess your credit conduct noting the type, age, number and value of the credit infractions on your credit file. These infractions can range from simple late payments, through to paid defaults, unpaid defaults, multiple defaults, judgements and writs, part IX agreement and bankruptcy. Using this information the non-conforming lender will classify the “risk profile” of your loan application and provide specific risk-based pricing.

In terms of borrowing limits, low deposit home loan options (95% lends) are available to those people with minor credit issues (ie. small paid default). If your credit conduct has larger or multiple credit infringements then a maximum 70% – 80% lending limit is likely possible.

If you are experiencing difficulties in getting a home loan due to poor credit conduct, please contact our experienced team and we'll explore all the options to find a solution that works for you.

Get started online or contact us for help

Here's our tips if you have poor credit

Select the appropriate lender

Although major banks have strict standards, non-conforming and specialist lenders tend to have a more lenient attitude towards individuals with bad credit. It is important to familiarize yourself with your credit report and take proactive measures to minimize any negative factors. Seeking guidance from a Zuu Money Finance Specialist can assist in selecting the right lender and home loan product to suit your needs.

Watch your Finances

Prevent the accumulation of more negative records on your credit report. Address any financial difficulties by:

Paying all your current commitments on time.

Try and pay off as many debts as you can.

Resolve any current default.

Avoid applying for any additional consumer finance.

Timing is important

It can be advantageous to wait for negative listings to be removed from your credit report before applying for a loan. However, purchasing property earlier could potentially be beneficial in terms of building equity. It is important to carefully assess the situation and if you are nearing the removal of a negative listing, it may be worth delaying your loan application to potentially secure better terms.

Get expert help

It may be possible to seek assistance from a qualified credit repair agency who can work with you to clear the listed defaults from your credit file. In addition, it’s always suggested that you seek independent accounting advice relating to your situation.

Frequently asked questions

I've got bad credit, does that mean I can't get a loan?

Absolutely not! Non-confirming lenders specialise in assisting individuals with bad credit to obtain finance and get their situation back on track. It's important to recognise that adverse credit is generally only possible with a reasonable deposit or substantial equity in an existing property. Talk to our team today about your unique financial position.

Can I refinance my tax debt?

Yes, there are a number of non-confirming lending options available that enable you to get back on top of your tax debt. Contact our team for assistance.

Why is the interest rate on a non-conforming loan higher?

In simple terms, the higher the risk to the lender, the higher the interest rate. If someone has struggled to meet repayments in the past, lenders view this as increased risk - and they price the loan accordingly.

Overtime as the individual continues to meet their regular repayment obligations the lender may reclassify the risk rating of the loan and offer a reduced interest rate.

How much can I borrow?

We’re all unique when it comes to our finances and borrowing needs. Your borrowing capacity is determined by your level of income and regular ongoing commitments. Contact us today and we can calculate your borrowing capacity based on your individual circumstances.

How much do I need for a deposit?

Minimum deposits for non-conforming loans can range from 5% to 40% of the value of a property depending on your credit history and current financial position. Speak with us to discuss your options for a deposit. You may be able to borrow against the equity in your existing home or an investment property.

How much will regular repayments be?

There are many different types of loan products with varying interest rates which will impact your repayment amount. Talk to us today about the products currently available that suit your lending needs, and we’ll calculate the repayments for you.

How often do I make home loan repayments — weekly, fortnightly or monthly?

Most lenders offer flexible repayment options to suit your pay cycle. Aim for weekly or fortnightly repayments, instead of monthly, as you will make more payments in a year, which will shave dollars and time off your loan.

What fees/costs should I budget for?

There are a number of fees and costs involved. To help avoid any surprises, the list below sets out many of the usual costs:

> Stamp duty — If purchasing this is the big one. All other costs are relatively small by comparison. Stamp duty rates vary between state and territory governments and also depend on the value of the property you buy. You may also have to pay stamp duty on the mortgage itself.

> Legal/conveyancing fees — If purchasing generally around $1,250 – $2000, these fees cover all the legal requirements around your property purchase, including title searches.

> Building inspection — This should be carried out by a qualified expert, such as a building inspector, before you purchase the property. Your Contract of Sale should be subject to the building inspection, so if there are any structural problems you have the option to withdraw from the purchase without any significant financial penalties. A building inspection and report can cost up to $1,000, depending on the size of the property.

> Pest inspection — Also to be carried out before purchase to ensure the property is free of problems, such as white ants. Your Contract of Sale should be subject to the pest inspection, so if any unwanted crawlies are found you may have the option to withdraw from the purchase without any significant financial penalties. Allow up to $800 depending on the size of the property.

> Lender costs — Most non-conforming lenders charge upfront establishment fees. We will let you know what your lender charges but allow about $500 to $3000.

> Moving costs — Don’t forget to factor in the cost of a removalist if you plan on using one.

> Mortgage Insurance costs — Non-conforming lenders will typically charge mortgage insurance or another risk fee based on the risk rating of the loan. Consult with our team about the risk fees that are applicable to your situation.

> Ongoing costs — You will need to include council and water rates along with regular loan repayments. It is important to also consider building insurance and contents insurance. Your lender will likely require a minimum sum insured for the building to cover the loan.

Hundreds of loans from Australia's top lenders

You don't need to run from bank-to-bank to find the best deal. Our team of mortgage specialist will compare hundreds of loans from Australia's top lenders and present you with a range of options that suit your lending needs.

Don't stress, We're here to help

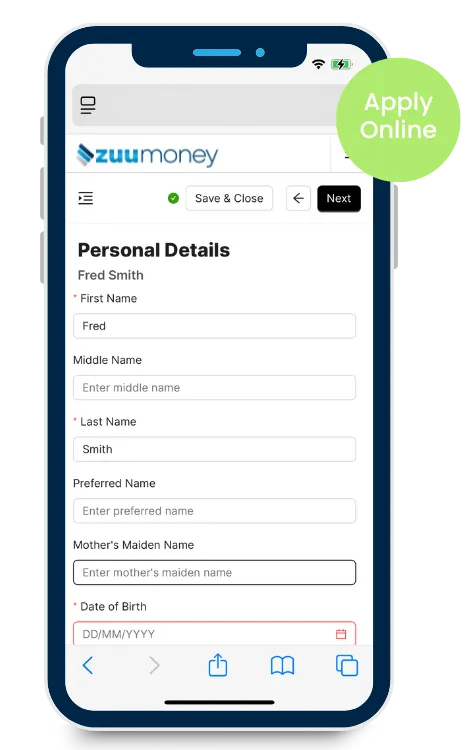

Applying for you next home loan has never been easier. The Zuu Money online application system allows you to enter your details from any device and upload your documents with ease.

Say goodbye to handwritten application forms and endless emails, all your information is collected in our simple, easy to use platform that saves you time and frustration.

You can get started online or contact your local Zuu Money Finance Specialist for assistance.

A service worthy of 5 stars

* Discounted rate available for owner occupied on Principal and Interest repayments with minimum loan size >$150,000 with borrowings <70%LVR. Rate subject to change without notice. Lender credit criteria, fees and charges apply. Zuu Money Pty Ltd does not endorse any particular lender. A product will be recommended based on your personal financial situation.

^ Comparison rate is calculated on a loan amount of $150,000 for a term of 25 years based on monthly repayments. Different amounts and terms will result in different comparison rates. Costs such as redraw fees or cost savings such as fee waivers, are not included in the comparison rate but may influence the cost of the loan.

Become a Broker

Zuu Money Pty Ltd ABN 66 670 119 105, Australian Credit Licence Number 567690.

Lender credit criteria, fees and charges apply.

The Zuu Money logo is a registered trademark of Zuu Money Pty Ltd. All rights reserved 2026.

| Terms and Conditions | Privacy Policy | Complaints